Winter 2023

Recent SEC and European Commission proposals require public companies to disclose extensive climate-related information, bringing more transparency to costs and greater urgency for properly detailed and relevant assessments.

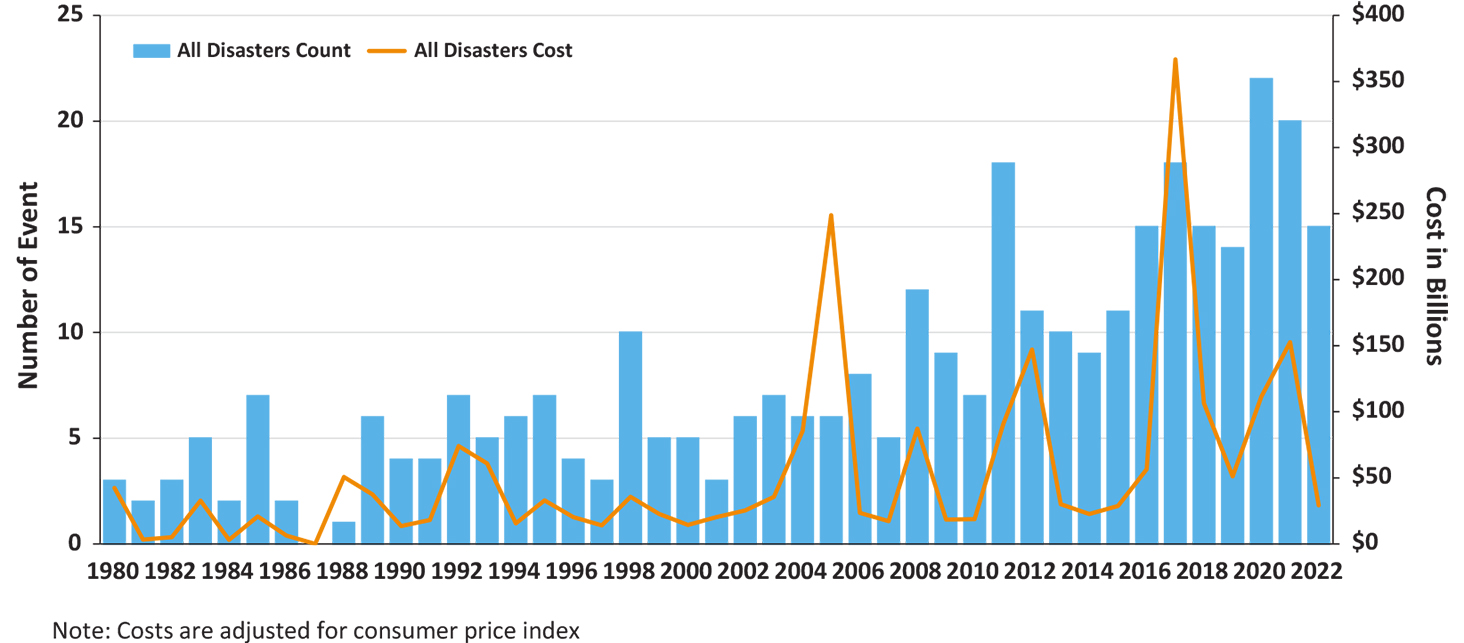

Twenty separate extreme weather and climate events (e.g., events with greater than $1 billion estimated loss) made 2021 the third most costly natural disaster year on record in the United States, behind 2017 and 2005. The total cost of these events was estimated at $152.6 billion (NOAA and NCEI, 2022). It is no secret that the frequency and total losses associated with such extreme weather events have been on the rise in recent decades (see Figure 1). The Sixth Assessment Report of the Intergovernmental Panel on Climate Change (IPCC) indicates that even under the most optimistic future climate scenario – which requires greenhouse gas (GHG) emissions to peak before 2025 and be reduced by 43 percent by 2030 to reach “net zero” by 2050 (IPCC, 2022) – more frequent severe weather events are expected in both short- and mid-term timeframes (IPCC, 2022).

It is no secret that the frequency and total losses associated with such extreme weather events have been on the rise in recent decades.”

On March 21, 2022, the Securities and Exchange Commission (SEC) proposed climate disclosure rules that would require most public companies to disclose extensive climate-related information in SEC filings (SEC, 2022). Similarly, earlier this year, the European Commission issued a proposal on corporate sustainability due diligence obligations to protect human rights and the environment (EC, 2022). Both of these proposals are part of a broader global sustainable investing trend, in which companies are required to disclose environmental, social, and governance (ESG) risk factors. The idea behind these proposals is to provide consistent, comparable, and reliable information and data to investors to enable informed judgments about the climate change impacts and opportunities of current and potential investments (SEC, 2022).

Climate-related risks can be divided into two categories: physical and transition risks (TCFD, 2017). Physical risks include acute and chronic risks. Acute physical risks are event-driven risks related to extreme weather events, such as hurricanes, floods, and wildfires. Chronic physical risks are risks that businesses may face as a result of more gradual changes, e.g., shifts in crop patterns and production due to gradual changes in temperature, precipitation, and sea level. Transition risks are risks related to the transition to a lower carbon-intensive economy, including policy and legal compliance, technology transition, and reputation risks. Both physical and transition risks can affect the financial performance of a company and would need to be disclosed under the proposed rules.

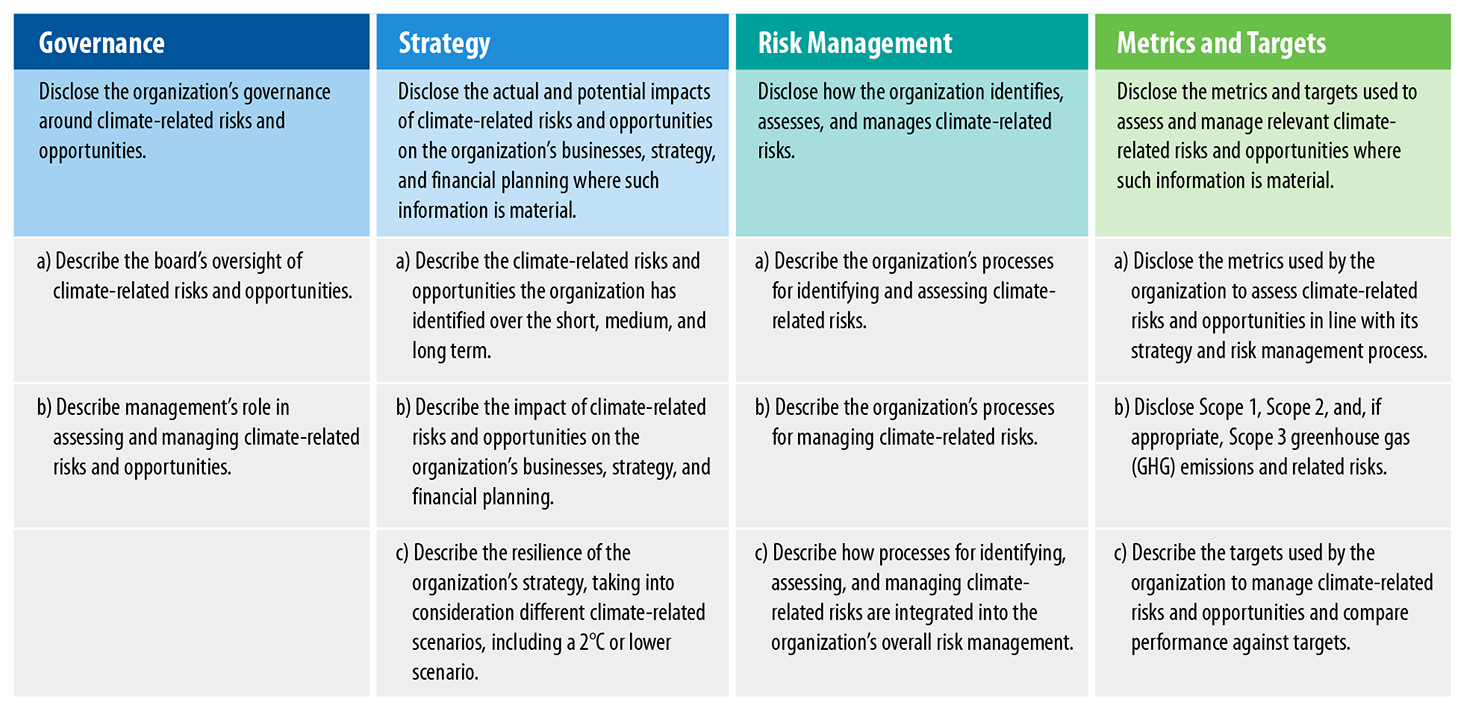

The SEC proposal (SEC, 2022) adapts the climate-related disclosure framework developed by the Task Force on Climate-related Financial Disclosures (TCFD, 2017) and requires disclosure in four categories: Governance, Strategy, Risk Management, and Metrics and Targets (see Figure 2). Under the Governance and Strategy categories, disclosures would inform investors and stakeholders on how climate-related issues are dealt with at the corporate leadership level.

The Risk Management and Metrics and Targets categories are quantitative disclosures, which would require input from climate scientists and engineers to be fulfilled properly. With respect to Risk Management, the reporting company would need to develop and present its methodologies for identifying, evaluating, and managing climate-related material risks. Moreover, the company’s risk management and transition plans must be disclosed in detail, including its metrics and targets (TCFD, 2017; SEC, 2022). With respect to impact metrics and targets, the proposed rules would require a reporting company to quantitatively disclose risks associated with climate-related events, such as flooding, drought, wildfires, extreme temperatures, and sea-level rise. For example, if a company’s materiality assessment finds that flooding presents a material risk to the company’s business, the proposed rule would require the reporting company to disclose the percentage of buildings, plants, and properties (in square meters or acres) that are located in flood hazard locations (SEC, 2022). Accurate reporting of these metrics requires direct contributions from climate experts and hydrologists to interpret the predictive climate model results and estimate relevant metrics. To produce meaningful and robust climate-related risk disclosures, technical experts interpret climate models and downscaled climate data (see Article 2 on downscaling); perform vulnerability and resiliency assessments; model secondary impacts of climate change (e.g., impact on air, water, and sediment quality); provide water availability/scarcity assessments; conduct GIS-based spatial analysis and visualization; and perform human health and ecological risk assessments.

The proposed rules would also require a reporting company to disclose its impact on climate change by reporting GHG emissions associated with its operations. Under the SEC proposal (SEC, 2022), direct emissions from sources that are controlled or owned by an organization (Scope 1 emissions) and indirect emissions associated with the purchase of electricity, steam, heat, or cooling (Scope 2 emissions) must be reported by all reporting companies. Additionally, in some cases, a reporting company may be required to disclose indirect GHG emissions from an asset it does not own or control but has an impact in its value chain (Scope 3 emissions). Fortunately, industry-specific carbon accounting frameworks and standards, such as GHG Protocol (WRI and WBCSD, 2022), are available and may be used to evaluate GHG emissions; however, specialized knowledge of the field or industry is often needed to use these standards appropriately. Additionally, the involvement of subject matter experts is necessary to set achievable emission targets and modify the processes and operations to achieve those targets.

The need for evaluation of climate-related financial risks originated from the financial sector’s movement towards more transparency regarding climate change impacts. Currently, climate-related risk reporting is conducted primarily by a reporting company’s in-house staff or its financial consultants, with limited input from scientists and engineers. However, as the proposed rules are finalized and put into effect, and as regulations become more stringent over time, scientists and engineers will be needed to perform robust, expert analyses to accurately assess climate change risk.

The author can be reached at aboroumand@gradientcorp.com.

European Commission (EC). 2022. “Proposal for a Directive of the European Parliament and of the Council on Corporate Sustainability Due Diligence and Amending Directive (EU) 2019/1937 (Text with EEA relevance).” COM(2022) 71 final; 2022/0051 (COD). 70p. February 23.

Intergovernmental Panel on Climate Change (IPCC). 2022. “The Evidence Is Clear: The time for Action Is Now. We Can Halve Emissions by 2030.” 5p. April 4.

National Oceanic and Atmospheric Administration (NOAA), National Centers for Environmental Information (NCEI). 2022. “U.S. Billion-Dollar Weather and Climate Disasters [Time Series Data].” Accessed on November 18, 2022, at https://www.ncei.noaa.gov/access/billions/time-series.

Task Force on Climate-related Financial Disclosures (TCFD). 2017. “Recommendations of the Task Force on Climate-related Financial Disclosures.” Submitted to Bank for International Settlements, Financial Stability Board. 74p. June.

US Securities and Exchange Commission (SEC). 2022. “The Enhancement and Standardization of Climate-Related Disclosures for Investors (Proposed Rule).” Fed. Reg. 87(69):21334-21473. 17 CFR 210; 17 CFR 229; 17 CFR 232; 17 CFR 239; 17 CFR 249. April 11.

World Resources Institute (WRI); World Business Council For Sustainable Development (WBCSD). 2022. “Greenhouse Gas (GHG) Protocol.” Accessed on November 18, 2022, at https://ghgprotocol.org/.